Guide to STAR Trusts in the Cayman Islands

The Special Trusts regime for Cayman Islands STAR trusts (now incorporated into Part VIII of the Trusts Act (As Revised)) provides the legal basis on which private purpose trusts can be established in the Cayman Islands, without affecting the previously existing laws governing the creation and administration of traditional trusts.

STAR trusts have gained a strong reputation for being flexible estate planning tools where special purpose vehicles are too inflexible or otherwise inappropriate. Unlike traditional English common law trust principles, under which a trust is not valid unless it is for the benefit of an identified person or class of persons or for charitable purposes, the STAR trusts can be (i) for the benefit of an identified person or any number of persons or (ii) solely for the benefit of charitable or non-charitable purposes or objectives provided that the purposes are lawful and not contrary to public policy.

1. What was the rationale for creating STAR Trusts?

Before the regime was introduced, it was not possible to create trusts for a purpose other than a charitable purpose. The STAR trusts regime also permits perpetual trusts; that is, trusts without a perpetuity or expiry period. Cayman Islands trusts which are not subject to the STAR trusts regime are currently limited to a maximum duration of 150 years.

As stated above, STAR trusts can be (i) for the benefit of an identified person or any number of persons, or (ii) solely for the benefit of charitable or non-charitable purposes or objectives provided that the purposes are lawful and not contrary to public policy. This is a unique feature of STAR trusts and highlights the flexibility offered by the STAR trust structure. It is a requirement of the STAR trust regime that at least one trustee of a STAR trust is a trust company licensed in the Cayman Islands or a private trust company registered as such in the Cayman Islands.

2. Key Features of STAR Trusts

i. The beneficiaries and/or objects may be persons, purposes or both. There may be any number of beneficiaries and any number of purposes, whether charitable or not, provided that such purposes/objects are lawful and not contrary to public policy.

ii. Any uncertainty as to the objects or mode of execution or administration of a STAR trust can be resolved by the Trustee (or any other person the STAR trust document so specifies) or by the Cayman court, if necessary. A STAR trust is therefore very unlikely to be declared void ab initio on grounds of uncertainty, as could be the case with a poorly drafted non-STAR trust.

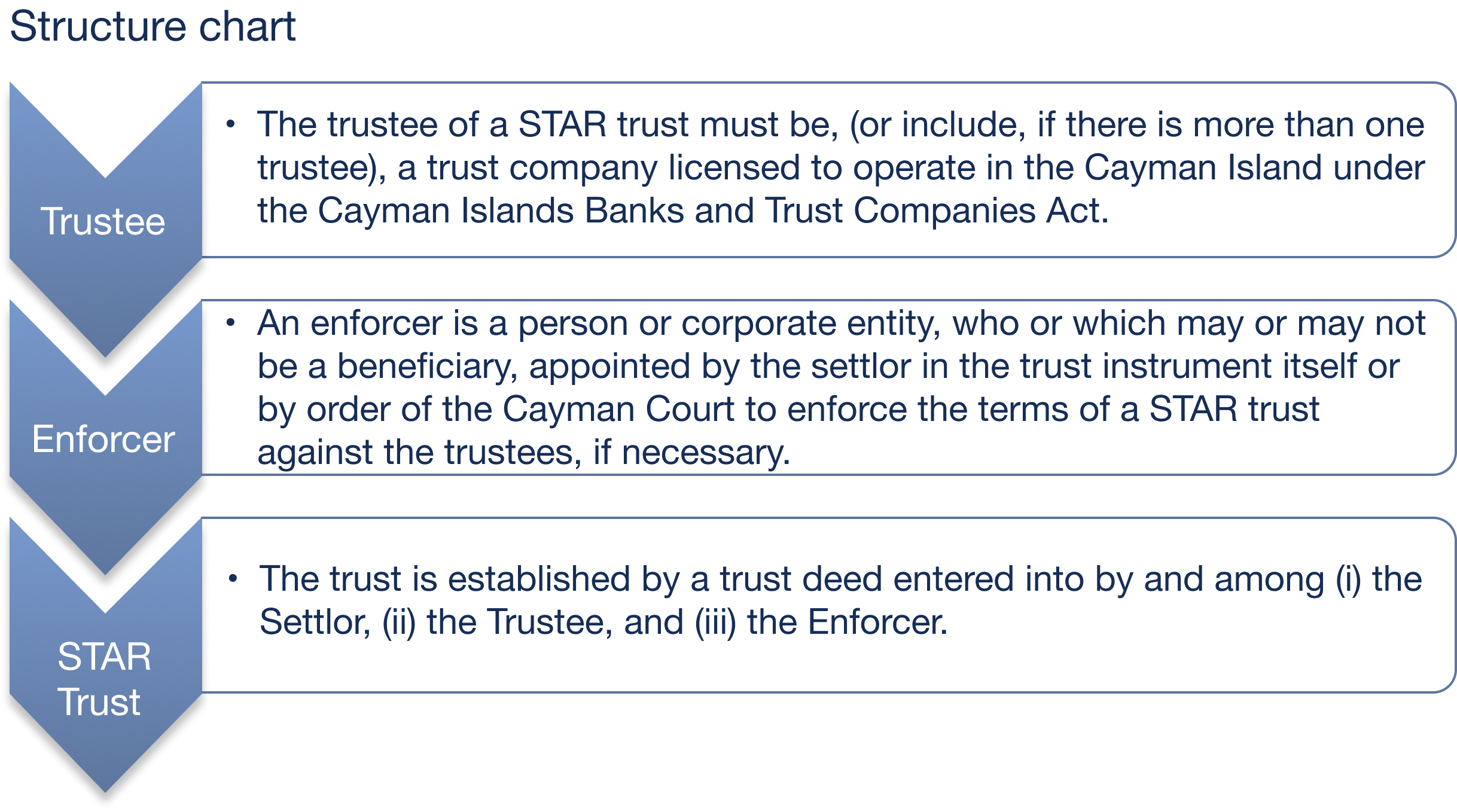

iii. The Trustee of a STAR trust must be or must include a trust company licensed to conduct trust business in the Cayman Islands. This adds a level of oversight and regulation above and beyond other jurisdictions. There are criminal sanctions attached if these requirements are overlooked or bypassed.

iv. STAR trusts must have an “Enforcer” who is the only individual person or corporate entity with legal standing to enforce the terms of the STAR trust. The STAR trust regime makes a clear distinction between the capacity to benefit from a STAR trust and the actual capacity to enforce such a trust. The effect is to remove rights of beneficiaries not only to enforce the trust, but also their right to seek disclosure of information regarding the trust and its ongoing administration.

v. The rule against perpetuities does not apply to STAR trusts, which may be created for an unlimited duration (or not, depending on the terms of the trust deed), which eliminates the risk of a resulting trust in favour of the settlor at the end of the perpetuity period and the adverse tax consequences which may flow from such an event.

vi. A STAR trust cannot hold land in the Cayman Islands but may hold an interest in a company, partnership or other entity which does.

3. What are STAR Trusts used for?

STAR trusts are commonly used for, among other things, the following.

1. To create dynasty-style trusts for multiple generations primarily for holding treasured family assets, investments, and preserving shares in family businesses.

2. To create trusts for philanthropic purposes which are outside of the scope of what would be considered charitable as a matter of Cayman Islands law.

3. To create trusts which restrict the rights of troublesome beneficiaries who may be tempted to challenge the trust, to seek to obtain information in relation to the trust, among other things.

4. To create trusts which are unrestricted by a perpetuity period.

5. To create trusts which benefit persons while at the same time achieving alternative objectives such as the continuation of family businesses.

6. To form “Special Purpose Vehicles” for a wide range of commercial transactions in a safe, flexible, and bankruptcy remote manner.

7. To act as a vehicle to hold shares in a private company, thus allowing a family member (or members) to retain a degree of control over the administration of the underlying trusts and influence decisions which may affect the underlying trusts and the assets they hold (most typically, shares in a family business).

8. For clubs and associations whereby their members can enforce terms of contracts without actually being a party to the contract. Also, upon the dissolution of the club or association, the contributed assets may be returned to members in portions specified in the trust deed, rather than in an ad-hoc manner.

4. Registration

The Trustee of a STAR trust must be or must include a trust company licensed to conduct trust business in the Cayman Islands. This adds a level of oversight and regulation above and beyond other jurisdictions.

The Trustee of a STAR trust is also required to keep, in its Cayman Islands office, a documentary record of:

i. the terms of the STAR trust,

ii. the identity of the Trustee and the enforcer(s),

iii. all settlements of the property upon trust and the identity of the settlor(s),

iv. the property subject to the STAR trust at the end of each of its accounting years, and

v. all distributions or applications of the trust property.

These additional obligations clarify any uncertainty in the common law regarding the retention of trust records and other vital information. These requirements therefore standardize and clarify important administrative expectations specifically imposed on STAR trust Trustees.

Registration

There is no requirement to register a STAR trust with the regulatory authorities in the Cayman Islands, hence confidentiality is preserved. In fact, all trust deeds (except “exempted trusts”) are exempt from registration. Therefore, the details of a STAR trust will remain confidential, subject only to disclosure as may be required by an order of the Cayman Islands courts.

Conclusion

With sound professional advice, the STAR trust provides a flexible and valuable tool for structured financing arrangements, as well as for the estate and financial planning of private parties seeking a safe and reliable trust mechanism to satisfy their specific needs and purposes.

Further Assistance

This publication is not intended to be a substitute for specific legal advice or a legal opinion. If you require further advice relating to the matters discussed in this Briefing, please contact us. We would be delighted to assist.

E: gary.smith@loebsmith.com

E: robert.farrell@loebsmith.com

E: ivy.wong@loebsmith.com

E. elizabeth.kenny@loebsmith.com

E: cesare.bandini@loebsmith.com

E: vivian.huang@loebsmith.com

E: faye.huang@loebsmith.com

E: yun.sheng@loebsmith.com

About Loeb Smith Attorneys

Loeb Smith is a leading offshore corporate law firm, with offices in the British Virgin Islands, the Cayman Islands, and Hong Kong, whose Attorneys have an outstanding record of advising on the Cayman Islands' law aspects and BVI law aspects of international corporate, investment, and finance transactions. Our team delivers high quality Partner-led professional legal services at competitive rates and has an excellent track record of advising investment fund managers, in-house counsels, financial institutions, onshore counsels, banks, companies, and private clients to find successful outcomes and solutions to their day-to-day issues and complex, strategic matters.

Recent News & Publications

14 Nov 2024

Preference shares and redemption rights in the Cayman Islands – an overview

View Full PDF

Background

It has become increasingly popular in recent years for venture capital (VC) and private equity (PE) firms to set up exempted companies limited by shares in the Cayman Islands for the purposes of pre-IPO equity...

Read More

14 Nov 2024

Preference shares and redemption rights in the Cayman Islands – an overview

View Full PDF

Background

It has become increasingly popular in recent years for venture capital (VC) and private equity (PE) firms to set up exempted companies limited by shares in the Cayman Islands for the purposes of pre-IPO equity...

Read More

4 Nov 2024

Cayman Islands: Guidance on inspections by CIMA

The Cayman Islands Monetary Authority conducts inspections to ensure that regulated entities comply with applicable laws and regulations. This is a general guide

Read More

4 Nov 2024

Cayman Islands: Guidance on inspections by CIMA

The Cayman Islands Monetary Authority conducts inspections to ensure that regulated entities comply with applicable laws and regulations. This is a general guide

Read More